If you’ve ever looked through a credit report, you may have come across the term DLA. At first glance, it seems like just another label. But the DLA on a credit report plays a much bigger part in your credit story than you might expect.

DLA stands for Date of Last Activity, and it marks the most recent action on a credit account — whether that’s a payment, a missed payment, or something a collector added. It might look like a small detail, but that date can decide how long an unpaid debt sticks to your record.

Knowing how the credit report DLA works can help you avoid trouble down the line. If it’s updated incorrectly, it could extend the life of a negative mark on your report. This can lower your score and delay your ability to qualify for a loan, apartment, or even a job.

In this article, you’ll learn:

- What DLA on a credit report really means?

- Why it’s one of the most misunderstood parts of credit reporting?

- How collectors might change it unfairly?

- How to correct it if the date looks wrong

Whether you’re fixing your own report or helping others, this guide will show you how to handle date of last activity credit report issues without getting overwhelmed.

Understanding the Date of Last Activity on a Credit Report

Grasping the meaning of the Date of Last Activity can make a real difference in how you manage your credit. While it may look like just another item on your report, the DLA on a credit report can impact how long accounts stay visible and how they influence your score.

By getting clear on how the credit report DLA works, you’re in a better position to catch reporting errors and take steps toward stronger financial health.

What Does DLA Mean on a Credit Report?

The Date of Last Activity, or DLA, is the most recent time something happened on an account. That might be a payment, a missed payment, or a note added by the creditor or collector. You’ll usually find the DLA listed alongside each account on your credit report.

Here’s a simple way to think about it:

- If you made a payment on a card in February, the DLA becomes February.

- If you stopped paying in April and nothing else happened, the DLA stays stuck at April.

That date matters because it often starts the clock for how long a negative account remains on your credit report — usually seven years.

Many people see DLA on a credit report and assume it’s just a timestamp. But in reality, it can influence your credit score and how lenders view you.

Why the Date of Last Activity Credit Report Section Is So Important?

The date of last activity credit report entry does more than sit in a report. It plays a major part in how your credit history is judged by lenders and how long negative records remain active.

Understanding how the DLA on a credit report functions gives you the chance to catch reporting mistakes early and take control of your credit timeline. It:

- Helps set the timeline for when a debt is removed

- Affects your credit score depending on how recent the activity was

- Can reset if the wrong party updates it without reason

If a collector changes that date unfairly, an old debt could appear newer than it really is. That’s a problem — because newer-looking debt hits your score harder and stays longer.

That’s why it’s important to track and understand how the credit report DLA is set, where it comes from, and who has the power to update it.

Who Controls the Credit Report DLA and Why It Matters?

The DLA on a credit report isn’t fixed permanently. Depending on who’s managing the account, this date can be updated — and those changes may impact how long a negative entry stays on your file.

Knowing who can modify the credit report DLA gives you a better chance at spotting errors or unfair updates before they affect your score.

Creditors and the Date of Last Activity

When an account is first opened, the creditor keeps track of every payment, late notice, or balance change. Each of these updates can trigger a new date of last activity credit report entry. In most cases, creditors set the original DLA when you either make a payment or miss one.

If you stay current, the DLA will reflect those regular payments. If you fall behind, the date becomes fixed at the last recorded activity.

That single entry — the DLA on a credit report — becomes a marker used to decide when the account should naturally fall off your record. Since the standard timeframe is seven years, an accurate DLA is vital for making sure that outdated debt doesn’t stick around longer than it should.

Debt Collectors and the Credit Report DLA

Once a debt changes hands and lands in collections, the new company may report a new line item. While the law prevents collectors from resetting the DLA without valid activity, some try to stretch the rules.

Contact from a collection agency, especially if you respond in writing, can be used — rightly or wrongly — to refresh the credit report DLA.

This tactic is called re-aging the debt, and it’s something consumers need to watch for. If done improperly, it may cause a negative account to remain on your report beyond its legal reporting window.

Knowing who reports the DLA — and how it can be changed — is the first step in protecting your report from outdated or unfair entries.

How Debt Collectors Can Change the DLA on a Credit Report?

Once a debt gets handed off to a collection agency, the way it’s reported can shift—sometimes unfairly. Debt collectors may attempt to change the DLA on a credit report by updating the account with new activity, even if that activity isn’t legitimate.

This tactic can make old debt seem more recent, affecting your credit score and keeping the account on your report longer than it should be.

Common Tactics Collectors Use to Re-Age Debt

Some collectors will report a newer date of last activity credit report entry without any actual payment or agreement from the consumer. This re-aging tactic can trick credit scoring systems into treating old debt as fresh.

It’s a method often used to pressure people into settling quickly, even when the debt is beyond the statute of limitations.

In some cases, the DLA on a credit report might be pushed forward just because a collector added a comment or updated the status. These subtle changes can reset the reporting timeline and give the impression that the debt is active when it’s not.

That’s why keeping an eye on the credit report DLA across all three bureaus is so important.

Consumer Rights and Protections

You’re not powerless. Under the Fair Credit Reporting Act (FCRA), collectors must have a valid reason to update the credit report DLA. If no payment has been made and no new agreement has been reached, changing the DLA is a violation.

If you spot this happening, you have the right to file a dispute. A well-prepared date of last activity dispute letter can be the first step to fixing it. When written correctly and backed by supporting documentation, this letter can result in a full correction or even deletion of the item.

Staying alert to updates in the date of last activity credit report section is one of the smartest things you can do to protect your credit.

How to Dispute and Fix DLA on a Credit Report?

When the DLA on a credit report is wrong, it can lead to unfair credit damage. Fortunately, you have the ability to correct it by using the proper steps.

Identifying inaccurate information in the date of last activity credit report section is the first move toward restoring accuracy.

Disputing errors and keeping your records up to date can help prevent old debts from showing up as new and dragging down your score.

Check for Incorrect DLA Entries

Start by reviewing your credit reports from all three major bureaus. Look at each account and focus on the date of last activity credit report section. If an account was paid off years ago but shows a recent DLA, it may have been re-aged.

A re-aged account can make old debt look recent, unfairly lowering your score. Review the credit report DLA entries across all bureaus to catch mismatches early and maintain a cleaner credit history.

Spotting these errors early helps you avoid unnecessary disputes. Consistent reviews of your DLA help ensure that outdated debts don’t resurface under new dates.

Send a Date of Last Activity Dispute Letter

If you notice a mistake, you have the right to challenge it. Send a date of last activity dispute letter to the credit bureau and the company that reported the debt. Your letter should explain why you believe the DLA is wrong and include any documents that back up your claim.

Make sure your explanation is clear and includes the correct DLA on a credit report based on your records. A precise, well-supported dispute can increase your chances of getting the entry corrected quickly.

Be specific about the correct date and reference any records that show when the last real activity took place. The clearer your documentation, the more likely your dispute will result in a successful correction.

Follow Up and Track the Outcome

Once the dispute is filed, the credit bureau must investigate and respond within 30 days. If they find the DLA on a credit report was incorrectly updated, they’re required to correct it.

Keep copies of everything you send, and check all three reports again after the investigation is complete. Verifying updates after a dispute helps confirm that the credit report DLA is now accurate.

Regular monitoring can also help you catch future issues with the date of last activity credit report section before they cause lasting harm. It’s wise to set a schedule for pulling your reports several times a year.

That way, any errors in the DLA can be spotted and addressed before they impact future applications.

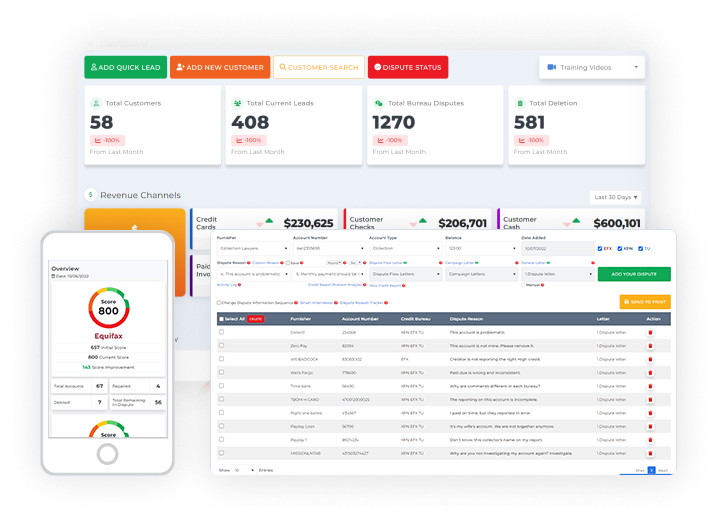

Simplify DLA Disputes with Client Dispute Manager Software

Disputing inaccurate information on your credit report can be overwhelming, especially when you’re trying to correct the DLA on a credit report. That’s where Client Dispute Manager Software comes in.

This tool is designed to make the process faster, easier, and more effective — whether you’re fixing your own report or helping others do the same.

With just a few steps, it helps you generate a proper date of last activity dispute letter, track dispute progress, and stay on top of changes to the credit report DLA.

Start Today and Explore the Features Firsthand!

Key Features That Help With Date of Last Activity Credit Report Issues

- Automated Dispute Generation: Create customized date of last activity dispute letters using built-in templates tailored for various scenarios.

- DLA Monitoring Tools: Identify suspicious changes in the DLA on a credit report and track discrepancies across bureaus.

- Client Tracking Dashboard: Manage multiple credit repair cases from one place and follow the status of every dispute.

- Integrated Credit Report Analysis: Pull and review credit data with built-in tools that highlight date of last activity credit report entries.

- Documentation Hub: Store and organize letters, responses, and credit bureau communications in one secure place.

Using Client Dispute Manager Software doesn’t just save time — it gives you a reliable system for protecting your credit or running a credit repair business.

If you’re serious about resolving credit report DLA issues and avoiding re-aged accounts, this software provides an advantage that manual processes can’t match.

Protecting Your Credit Health After a DLA Dispute

Fixing an incorrect DLA on a credit report is an important step — but protecting your credit going forward matters just as much. Once you’ve submitted a date of last activity dispute letter and seen the correction take place, it’s smart to focus on building habits that keep your credit report accurate and your score moving in the right direction.

The tips below can help you maintain momentum and prevent future issues with your credit report DLA.

How to Maintain a Positive Payment History?

Your payment history is the most powerful factor in your credit score. After resolving a date of last activity credit report issue, make sure to stay current on all your accounts. Set up automatic payments or reminders to avoid missed due dates. Even one late payment can restart a negative DLA and bring down your score.

Keeping accounts in good standing also protects the DLA on a credit report from being altered by new negative activity.

Paying at least the minimum amount by the due date every month helps ensure your record stays clean and accurate. Over time, steady on-time payments help older negative DLAs fade into the background of your credit profile.

The more consistent your payments, the less weight older delinquencies carry in scoring models. A stable payment pattern also makes it harder for errors in the credit report DLA to significantly impact your score.

How Often to Check Your DLA on Credit Report?

It’s a good idea to review your credit report DLA entries at least twice a year. Checking regularly lets you spot errors early — before they lead to bigger problems. Look specifically at accounts in collections or those with no recent activity. These are the most likely to show suspicious updates.

You can access a free credit report from each of the three major bureaus once a year. Spread these checks out every four months to monitor your date of last activity credit report throughout the year. If anything looks off, take screenshots, gather proof, and get ready to dispute it again.

Frequent monitoring helps you detect unauthorized changes and ensures that the DLA on a credit report stays consistent across all reporting agencies. Even small inconsistencies can lead to score differences that affect credit decisions.

Tips for Avoiding DLA Manipulation in the Future

Collectors sometimes use tricky methods to reset the DLA on a credit report. Avoid phone calls or written acknowledgments of debts that are beyond the statute of limitations. These actions could be misused as an excuse to re-age the account.

Instead, keep all communication in writing, and only respond when you fully understand your rights. Before agreeing to pay or settle a debt, make sure the credit report DLA won’t be unfairly refreshed.

Staying informed, asking questions, and reviewing your reports consistently are the best ways to avoid future manipulation of your date of last activity credit report.

Also, be cautious with any online portals collectors may offer, as even logging in could be considered activity. The best way to protect yourself is to treat every interaction as official and document everything.

FAQs About DLA on a Credit Report

What Is DLA on a Credit Report?

DLA, or Date of Last Activity, refers to the most recent activity reported on a credit account. This could include a payment, a missed payment, or even an update made by a debt collector. The DLA on a credit report is used to determine how long an account will remain visible, especially if it is negative.

Inaccurate updates to this date can make a debt appear more recent than it truly is, which can negatively impact your score and delay the account’s removal from your credit file.

Does DLA Affect Credit Score?

Yes, the DLA on a credit report can influence your credit score. If the most recent activity was negative—such as a missed payment or collection action—this will be reflected in your score.

The newer the date of last activity credit report entry appears, the more impact it typically has on how lenders evaluate your creditworthiness. Keeping this date accurate is essential to avoid unnecessary damage to your credit profile.

What Does DLA Mean in Finance?

In the context of credit reporting, DLA stands for Date of Last Activity. It refers to the most recent transaction or update on a credit account. This includes any payment, charge, adjustment, or reporting change.

The credit report DLA is crucial for determining when derogatory accounts are scheduled to fall off your report and how active your debt appears to lenders and credit scoring models.

What Does DFD/DLA Mean on a Credit Report?

DFD means Date First Delinquent, while DLA stands for Date of Last Activity. The DFD marks the point when an account first became past due and stayed that way, while the DLA reflects the most recent activity on that account—good or bad.

Both fields are essential in determining the age and status of a debt. Together, the DFD and DLA on a credit report provide important context for how an account is handled by creditors and collection agencies.

Can DLA Affect When Items Drop Off?

Absolutely. The date of last activity credit report entry often determines when a negative item is scheduled to be removed from your credit history—typically after seven years.

If the DLA is updated or re-aged (especially by a collection agency), the countdown may restart, keeping the item on your report longer than allowed.

This is why it’s critical to monitor the DLA on a credit report and dispute any unauthorized changes that could extend the life of a negative account.

How Often Should You Check Your Credit Report DLA?

It’s wise to check your credit report DLA at least twice a year. Regular monitoring allows you to spot discrepancies early and correct any errors before they harm your score. Focus particularly on older debts, settled accounts, and items in collections.

If you notice an unexpected update to the date of last activity credit report field, investigate immediately and be prepared to dispute it. Staying proactive is the key to maintaining an accurate and healthy credit file.

Conclusion: Take Control of the DLA on Your Credit Report

Understanding the DLA on a credit report gives you a powerful edge when it comes to managing your credit. While the Date of Last Activity may seem like just a technical detail, it can directly affect your credit score, how long negative accounts remain visible, and whether old debts are misrepresented as new.

Left unchecked, an incorrect credit report DLA can delay financial recovery and cause long-term damage.

Now that you know what the date of last activity credit report entry means and how it’s used, you can take steps to review your credit files, detect potential errors, and dispute any inaccurate updates.

Whether you’re doing this for yourself or helping others through a credit repair business, staying informed is essential.

If you want to make the dispute process more efficient, using software like Client Dispute Manager can simplify everything — from tracking changes to sending a proper date of last activity dispute letter. It’s a smart way to take action with confidence.

The key takeaway? Monitor your reports, know your rights, and act quickly when something doesn’t look right. With the right tools and information, you’re in control of your credit report DLA — not the other way around.

Mark Clayborne

Mark Clayborne specializes in credit repair, starting and running credit repair businesses. He's passionate about helping businesses gain freedom from their 9-5 and live the life they really want. You can follow him on YouTube.

Below Is More Content For Your Review: