![Starting a Credit Repair Business in Pennsylvania [2026]](https://clientdisputemanagersoftware.com/wp-content/uploads/2023/05/Starting-a-Credit-Repair-Business-in-Pennsylvania-2026.jpg)

Starting a credit repair business in Pennsylvania can be a legitimate and profitable opportunity but only if it is done within a tightly regulated legal framework. Unlike many service-based businesses, credit repair companies operate under both federal law and Pennsylvania-specific regulations, and failing to follow those rules can result in fines, shutdowns, or legal action.

Pennsylvania treats credit repair as a consumer-protection driven industry, which means business owners must meet strict requirements related to contracts, disclosures, record keeping, and surety bonding before working with clients. Simply registering a business or creating a website is not enough to operate legally in this state.

This guide explains exactly what it takes to start a credit repair business in Pennsylvania, including the laws that apply, bonding and registration requirements, and the step-by-step process to launch in a compliant way. Whether you are new to the credit repair industry or looking to expand into Pennsylvania, this article will help you understand the legal expectations before you begin.

Is Starting a Credit Repair Business in Pennsylvania Legal?

Yes, starting a credit repair business in Pennsylvania is legal, but only if the business complies with both federal credit repair laws and Pennsylvania’s consumer protection regulations. Credit repair is not a lightly regulated activity in this state, and businesses that operate outside the law can face fines, enforcement actions, or forced closure.

Pennsylvania allows credit repair services to operate under the Pennsylvania Credit Services Act, which exists to protect consumers from deceptive or abusive practices. This law sets strict rules around how credit repair companies advertise, contract with clients, collect payments, and document their services.

In addition to state law, all Pennsylvania credit repair businesses must also comply with federal regulations such as the Credit Repair Organizations Act (CROA).

It is important to understand that credit repair legality in Pennsylvania is conditional. You cannot legally operate by simply forming an LLC or offering “credit help” services online. Businesses must meet specific compliance requirements before working with clients, including proper disclosures, written agreements, and in many cases, securing a surety bond.

For entrepreneurs willing to follow these rules, Pennsylvania provides a clear legal path to operate a compliant credit repair business. For those who ignore them, the risks are significant. Understanding the legal framework upfront is the most important step before launching.

Federal Credit Repair Laws You Must Follow in Pennsylvania

Before looking at Pennsylvania-specific requirements, every credit repair business must understand that federal law applies in all 50 states, including Pennsylvania. These laws define what credit repair companies can and cannot do, regardless of where the business is located or registered.

Failing to follow federal credit repair laws can result in enforcement actions, consumer lawsuits, and permanent business shutdowns even if your business complies with state rules.

Credit Repair Organizations Act (CROA)

The Credit Repair Organizations Act (CROA) is the primary federal law governing credit repair businesses. It exists to prevent deceptive practices and protect consumers seeking help with their credit.

Under CROA, Pennsylvania credit repair businesses must:

- Prohibit Advance Fees: You cannot charge clients before services are fully performed.

- Use Written Contracts: Every client must receive a written agreement outlining services, timelines, and fees.

- Provide Mandatory Disclosures: Clients must be informed of their rights, including their ability to dispute credit report errors on their own.

- Honor the Right to Cancel: Consumers have a legally protected cancellation window after signing a contract.

Violating CROA is one of the fastest ways to face federal penalties in the credit repair industry.

Other Federal Laws That Apply to Credit Repair Businesses

In addition to CROA, credit repair companies in Pennsylvania must operate in alignment with several other federal consumer protection laws, including:

- Fair Credit Reporting Act (FCRA): Governs how credit information is reported, corrected, and disputed.

- Fair Debt Collection Practices Act (FDCPA): Applies when credit repair services intersect with debt collection or creditor communications.

- Equal Credit Opportunity Act (ECOA): Prohibits discrimination in credit-related services.

These laws influence how disputes are submitted, how client information is handled, and how services are marketed.

Federal compliance is not optional. Pennsylvania-specific rules build on top of these laws, not around them. Understanding this foundation is essential before moving forward with state registration or bonding requirements.

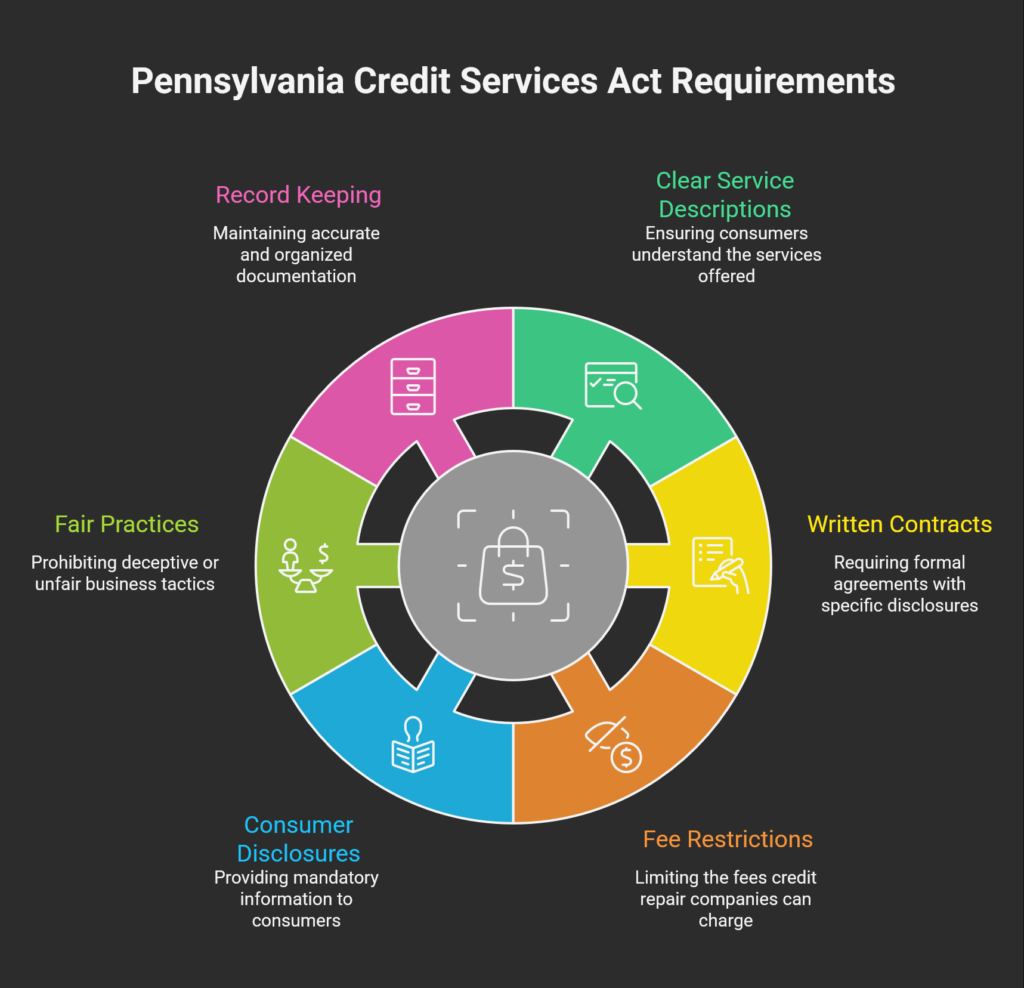

Pennsylvania Credit Services Act (CSA) Requirements

In addition to federal regulations, credit repair businesses operating in Pennsylvania must comply with the Pennsylvania Credit Services Act (CSA). This law applies to any business that offers services to improve, repair, or modify a consumer’s credit record for a fee, regardless of where the business is physically located.

Under the CSA, credit repair companies are classified as credit services organizations and must follow specific consumer protection rules designed to prevent misleading or abusive practices.

Key Requirements Under the Pennsylvania Credit Services Act

Pennsylvania credit repair businesses are generally required to:

- Provide Clear and Accurate Descriptions of Services

- Use Written Contracts With Specific Disclosures

- Comply With Fee and Payment Restrictions

- Include Mandatory Consumer Disclosures

- Avoid Deceptive or Unfair Business Practices

- Maintain Proper Records and Documentation

Why Pennsylvania Credit Services Act (CSA) Compliance Matters?

Failure to comply with the Pennsylvania Credit Services Act can result in:

- Civil penalties and fines

- Contract voiding and refund obligations

- Enforcement actions by state authorities

- Legal exposure from consumer lawsuits

Even businesses that fully comply with federal credit repair laws can still face penalties if Pennsylvania-specific requirements are ignored. CSA compliance is a foundational requirement not an optional step.

Pennsylvania Credit Repair Surety Bond Requirements

Most credit repair businesses operating in Pennsylvania are required to secure a credit repair surety bond before offering services to consumers. This bond is a critical consumer protection mechanism and one of the most commonly overlooked legal requirements by new credit repair companies.

A surety bond is not insurance for the business owner. Instead, it exists to protect consumers in the event that a credit repair company violates the Pennsylvania Credit Services Act or engages in unlawful or deceptive practices.

Key Surety Bond Requirements in Pennsylvania

Pennsylvania credit repair businesses are generally required to:

- Obtain a Credit Repair Surety Bond Before Operating

- Maintain the Bond for the Duration of Business Operations

- Ensure the Bond Meets State-Specified Coverage Amounts

- Provide Proof of Bonding When Requested by Regulators or Clients

The required bond amount in Pennsylvania typically falls within a state-defined range, depending on the nature and scope of services offered. Bond amounts are subject to change and should be verified with the appropriate state authority before launching operations.

What Happens If You Operate Without a Bond?

Operating a credit repair business in Pennsylvania without the required surety bond can result in:

- Immediate Enforcement Action by State Authorities

- Fines and Civil Penalties

- Contract Invalidations and Forced Refunds

- Business Shutdown or Suspension

Securing the appropriate surety bond is not a formality it is a prerequisite for legally operating a credit repair business in Pennsylvania. Businesses should complete this step before signing clients or collecting any fees.

Business Registration Requirements in Pennsylvania

Before offering credit repair services in Pennsylvania, you must properly register your business and establish a compliant legal structure.

Registration alone does not authorize you to operate as a credit repair company, but it is a required foundational step before securing bonding, contracts, and client agreements.

Register With the Pennsylvania Department of State

Most credit repair businesses in Pennsylvania operate as a limited liability company (LLC) or a corporation. While sole proprietorships are possible, they often expose owners to unnecessary personal liability in a highly regulated industry.

When selecting a structure, consider liability protection, tax treatment, and long-term scalability.

To operate legally, you must register your business with the Pennsylvania Department of State. This process formally establishes your entity and allows you to conduct business within the state.

Registration typically includes:

- Selecting and Registering a Business Name

- Filing Formation Documents With the State

- Designating a Registered Office or Registered Agent

Business names should avoid misleading language that could imply guaranteed credit outcomes or government affiliation.

Common Compliance Mistakes Pennsylvania Credit Repair Businesses Make

Many credit repair businesses in Pennsylvania run into legal trouble not because of bad intentions, but because they misunderstand or overlook key compliance requirements. These mistakes can lead to fines, contract disputes, refunds, or enforcement actions that are difficult to recover from.

Most Common Credit Repair Compliance Mistakes

Pennsylvania credit repair businesses frequently make the following errors:

- Charging Fees Before Services Are Fully Performed: Collecting advance fees violates federal law and can invalidate client contracts.

- Using Non-Compliant or Incomplete Client Contracts: Missing disclosures, vague service descriptions, or incorrect cancellation terms can render agreements unenforceable.

- Operating Without a Required Surety Bond: Failing to secure or maintain a bond when required can result in immediate penalties or shutdowns.

- Making Guaranteed or Misleading Marketing Claims: Promises such as “guaranteed score increases” or “instant credit fixes” can trigger regulatory scrutiny.

- Poor Recordkeeping and Dispute Documentation: Inadequate documentation makes it difficult to defend your business if a consumer complaint is filed.

- Ignoring Pennsylvania-Specific Consumer Protection Rules: Compliance with federal law alone is not sufficient when operating in Pennsylvania.

Avoiding these mistakes requires a compliance-first mindset from day one. Businesses that prioritize legal structure and documentation are far more likely to operate sustainably in Pennsylvania’s regulated credit repair environment.

Tools & Systems for Managing a Compliant Credit Repair Business

Running a compliant credit repair business in Pennsylvania requires more than legal knowledge. Businesses must also maintain accurate records, track disputes properly, and ensure timelines align with federal and state requirements.

Without reliable systems in place, even well-intentioned businesses can fall out of compliance. Many credit repair companies use dedicated tools and internal systems to help manage daily operations and reduce compliance risk.

Why Systems Matter in Credit Repair?

Effective tools and workflows help businesses:

- Track Client Disputes and Progress Accurately

- Maintain Documentation for Each Client File

- Monitor Service Timelines and Completion Status

- Store Contracts, Disclosures, and Communication Records

- Respond Efficiently to Client Questions or Complaints

Proper documentation is especially important in regulated industries, where businesses may be required to demonstrate compliance during audits or dispute reviews.

How Client Dispute Manager Software Supports Pennsylvania Credit Repair Businesses?

As a credit repair business grows, managing compliance manually becomes increasingly difficult. Pennsylvania credit repair companies are required to maintain accurate records, document disputes, track service timelines, and store client agreements in a way that can withstand regulatory or consumer scrutiny.

This is where tools like Client Dispute Manager Software are commonly used to support compliant operations.

Key Features of Client Dispute Manager Software That Support Compliance

Client Dispute Manager Software is designed to help credit repair businesses manage operations in a structured and defensible way. Core features typically include:

- Centralized Client File Management: Keeps all client information, agreements, and service history organized in one secure location.

- Credit Dispute Tracking and Status Monitoring: Allows businesses to track when disputes are created, submitted, updated, and resolved, helping demonstrate that services were actually performed.

- Contract and Disclosure Storage: Supports storing signed client agreements, required disclosures, and cancellation notices for record keeping and compliance reference.

- Service Timeline Monitoring: Helps ensure services align with agreed timelines and reduces the risk of improper billing or advance fee violations.

- Communication and Activity Logs: Maintains a record of client communications and actions taken, which can be critical if a complaint or dispute arises.

- Document Upload and Management: Allows supporting documents, credit reports, and correspondence to be attached directly to client files for audit readiness.

- Multi-Client Workflow Organization: Helps businesses manage multiple client accounts consistently without relying on spreadsheets or manual tracking.

- Compliance-Focused Operational Structure: Encourages standardized processes that reduce human error and improve internal accountability.

Start Today and Explore the Features Firsthand!

Frequently Asked Questions About Credit Repair in Pennsylvania

Is Credit Repair Legal in Pennsylvania?

Yes, credit repair is legal in Pennsylvania. However, businesses must comply with federal credit repair laws and the Pennsylvania Credit Services Act. Operating without meeting these requirements can result in fines, enforcement actions, or business shutdowns.

Do I Need a License or Bond to Start a Credit Repair Business in Pennsylvania?

Pennsylvania does not issue a traditional “license” for credit repair businesses, but many credit services organizations are required to obtain a credit repair surety bond and comply with state registration and disclosure rules before operating.

How Much Is the Credit Repair Surety Bond in Pennsylvania?

The required bond amount in Pennsylvania typically falls within a state-defined range, depending on the business model and services offered. Bond requirements should be verified with the appropriate state authority before launching operations.

Can I Start a Credit Repair Business From Home in Pennsylvania?

Yes, a credit repair business can be operated from home in Pennsylvania, provided it complies with all federal and state laws, maintains proper records, and meets bonding and disclosure requirements. Zoning or local business rules may also apply.

Is Client Dispute Manager Software Suitable for New Credit Repair Businesses?

Yes. Many new credit repair businesses use structured software early to avoid manual errors, improve organization, and establish compliant workflows from the beginning. Others adopt software as their client volume grows.

Final Thoughts: Build Compliance First, Then Grow

Starting a credit repair business in Pennsylvania is a legitimate opportunity, but it is not a casual or lightly regulated venture. Federal laws and the Pennsylvania Credit Services Act impose clear obligations on how credit repair services are marketed, contracted, delivered, and documented.

Businesses that overlook these requirements risk fines, refunds, enforcement actions, or permanent closure.

The most successful credit repair companies in Pennsylvania are those that prioritize compliance before growth. That means understanding the legal framework, securing required bonding, using compliant contracts and disclosures, and maintaining accurate records from day one. Growth should come after structure not before it.

Tools and systems can help support compliant operations, but no software or shortcut replaces a solid understanding of the law and responsible business practices. Business owners remain accountable for every service provided and every representation made to clients.

By approaching credit repair with a compliance-first mindset, entrepreneurs can build businesses that are not only lawful, but sustainable, credible, and positioned for long-term success in Pennsylvania’s regulated environment.

Mark Clayborne

Mark Clayborne specializes in credit repair, starting and running credit repair businesses. He's passionate about helping businesses gain freedom from their 9-5 and live the life they really want. You can follow him on YouTube.

Start Today and Explore the Features Firsthand!

Below Is More Content For Your Review: