Are you struggling with student loan debt that’s dragging down your credit score? You’re not alone. Millions of Americans are burdened by student loans, but the good news is that there are ways to remove student loans from your credit report. In this article, we’ll explore the steps you can take to improve your credit and get back on track financially.

Start Today and Explore the Features Firsthand!

Understanding Student Loans and Credit Reports

Before we dive into how to remove student loans from credit report, let’s first understand how they impact your credit. Student loans are considered installment loans, meaning you borrow a fixed amount and pay it back over a set period of time. Like other types of debt, student loans can have a significant impact on your credit score, especially if you miss payments or default on the loan.

When you take out a student loan, the lender reports the account to the three major credit bureaus – Equifax, Experian, and TransUnion. This information becomes part of your credit report, which is used to calculate your credit score. Late payments, defaults, and other negative actions related to your student loans can all lower your credit score.

How Student Loans Affect Your Credit Score?

Your credit score is a three-digit number that represents your creditworthiness. It’s based on the information in your credit report, including your payment history, credit utilization, length of credit history, types of credit used, and recent credit inquiries.

Student loans can impact your credit score in several ways:

- Payment History: Your payment history is the most important factor in your credit score, accounting for 35% of the total. Late payments, missed payments, and defaults on your student loans can significantly lower your score.

- Credit Utilization: Your credit utilization is the amount of credit you’re using compared to your credit limits. While student loans don’t typically have a credit limit, high loan balances can still impact your overall credit utilization and lower your score.

- Length of Credit History: The length of your credit history makes up 15% of your credit score. If you have older student loans that you’ve been paying on time, they can actually help your score by demonstrating a long history of responsible credit use.

- Credit Mix: Having a mix of different types of credit (such as credit cards, mortgages, and student loans) can actually be good for your score, as it shows that you can manage different types of debt responsibly.

Strategies for Removing Student Loans from Your Credit Report

So, how can you remove student loans from credit report and improve your credit? Here are some strategies to consider:

Dispute Inaccurate Information

If you find errors or inaccuracies on your credit report related to your student loans, you have the right to dispute them. This could include incorrect payment amounts, late payments that were actually on time, or loans that don’t belong to you. To dispute an error, you’ll need to contact the credit bureau(s) reporting the inaccurate information and provide documentation to support your claim.

Start Today and Explore the Features Firsthand!

Seek Loan Forgiveness or Discharge

In some cases, you may be eligible for student loan forgiveness or discharge, which could result in the loan being removed from your credit report. Some common scenarios include:

- Total and Permanent Disability Discharge: If you become permanently disabled and unable to work, you may qualify to have your federal student loans discharged.

- Public Service Loan Forgiveness: If you work full-time for a government organization or non-profit, you may be eligible for loan forgiveness after making 120 qualifying payments.

- Closed School Discharge: If your school closed while you were enrolled or shortly after you withdrew, you may be eligible for loan discharge.

- Borrower Defense to Repayment: If your school misled you or engaged in misconduct, you might be eligible for loan forgiveness under the borrower defense to repayment rule.

- Teacher Loan Forgiveness: If you teach full-time for five consecutive years in a low-income school or educational service agency, you may be eligible for up to $17,500 in loan forgiveness.

To learn more about these and other loan forgiveness and discharge options, visit the Federal Student Aid website.

Consider Loan Rehabilitation

If you’ve defaulted on your federal student loans, you may be able to remove the default from your credit report through loan rehabilitation. This process involves agreeing to make nine voluntary, on-time payments over a period of 10 consecutive months. Once you’ve made all nine payments, the default will be removed from your credit report, although the late payments leading up to the default will remain.

Consolidate Your Loans

If you have multiple federal student loans, consolidating them into a single Direct Consolidation Loan can help simplify your repayment and potentially lower your monthly payments. While consolidation won’t remove the loans from your credit report, it can make them easier to manage and help you avoid missed or late payments that could damage your credit.

Pay Off Your Loans

Of course, the most straightforward way to remove student loans credit report is to pay them off in full. Once your loans are paid off, the accounts will be marked as “paid in full” on your credit report. While this won’t remove the loans from your credit history entirely, it will show that you successfully paid off the debt, which can have a positive impact on your credit score over time.

Start Today and Explore the Features Firsthand!

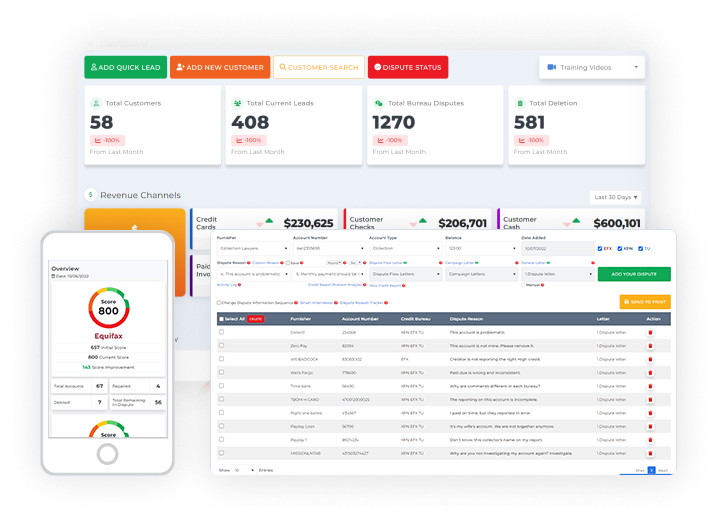

Using Client Dispute Manager Software to Remove Student Loans from Credit Reports

If you’re running a credit repair business, you know how important it is to have a system in place for managing client disputes. That’s where Client Dispute Manager Software comes in.

Client Dispute Manager Software is a specialized tool designed to help credit repair professionals streamline the dispute resolution process. It allows you to track and manage disputes, communicate with clients and credit bureaus, and generate important documents and reports.

Here’s how it can assist in the process:

- Identifying Inaccurate Student Loan Information: The software can automatically pull credit reports and highlight potential errors related to student loans, such as incorrect balances, duplicate entries, or loans that have been paid off but still show as active.

- Generating Dispute Letters: Once inaccuracies are identified, the software can generate customized dispute letters to send to credit bureaus. It pulls in relevant client and loan information to create a strong case for removal.

- Tracking Dispute Progress: The software provides a centralized dashboard to track the status of all student loan disputes, including when they were filed, responses received, and outcomes achieved. It can also alert you when follow-up is needed.

- Communicating with Clients: Keep clients informed and engaged by sending automated updates and personalized messages directly through the software. Share dispute filing confirmations, credit bureau responses, and next steps.

- Leveraging Data and Analytics: Use the software’s data and analytics capabilities to track success rates, resolution times, and client satisfaction. Identify areas for improvement and demonstrate your expertise to potential clients.

By streamlining and automating key aspects of the student loan dispute process, Client Dispute Manager Software can help you achieve better outcomes for your clients and grow your credit repair business. Whether you’re working to remove a cosigner from a student loan or remove student loans from credit report without paying, this tool can be a valuable asset in your toolkit.

Frequently Asked Questions (FAQs)

How Long Do Student Loans Stay On Your Credit Report?

Student loans remain on your credit report for seven years from the date of default or final payment, whichever is later. If you’ve paid off your loans on time and in full, they can actually have a positive impact on your credit score by demonstrating a history of responsible borrowing and repayment.

Start Today and Explore the Features Firsthand!

Can Private Student Loans Be Removed From Your Credit Report?

Private student loans are subject to the same credit reporting rules as other types of installment loans. This means they can only be removed from your credit report if they were reported in error or if you’ve successfully negotiated with the lender or collections agency to have them removed in exchange for payment. However, negative marks related to private student loans should fall off your credit report after seven years.

How Can I Remove A Cosigner From A Student Loan On My Credit Report?

If you have a cosigner on your student loan, they’re equally responsible for repaying the debt and their credit will be impacted by late payments or default. To remove a cosigner from your loan and credit report, you typically have two options:

- Refinance The Loan In Your Name Only: If you have good credit and a stable income, you may be able to refinance your student loan without a cosigner. This would remove the cosigner’s obligation and their name from the credit report.

- Apply For Cosigner Release: Some lenders offer cosigner release programs, which allow you to remove your cosigner after making a certain number of on-time payments (usually 12-48). Check with your lender to see if this option is available and what the requirements are.

Is It Possible To Remove Student Loans From Credit Report Without Paying?

In most cases, no. Student loans are legal obligations, and lenders have the right to report accurate information about your accounts to the credit bureaus. The only way to remove student loans from your credit report without paying is if they were reported in error or if you qualify for loan forgiveness or discharge due to special circumstances like school closure, disability, or death.

Conclusion

Removing student loans from credit reports can be a complex and time-consuming process, but Client Dispute Manager Software can help streamline and automate many of the key steps. By identifying inaccuracies, generating dispute letters, tracking progress, communicating with clients, and leveraging data, this powerful tool can help you achieve better outcomes for your clients and grow your credit repair business.

Whether you’re helping clients remove a cosigner from a student loan or working to remove student loans from credit report without paying, Client Dispute Manager Software can be a valuable addition to your toolkit. With the right technology and strategies, you can make a real difference in your clients’ financial lives and set your business up for long-term success.

Mark Clayborne

Mark Clayborne specializes in credit repair, starting and running credit repair businesses. He's passionate about helping businesses gain freedom from their 9-5 and live the life they really want. You can follow him on YouTube.

Start Today and Explore the Features Firsthand!

Below Is More Content For Your Review:

- Navigating Credit Reports: How to Dispute Inaccurate Items Effectively

- How Credit Repair Software Eliminates Errors & Disputes